Accounting records – a rich source of knowledge

In most institutions or public agencies, it was important to document how available funds were spent. In many archives, accounting records are the most abundant type of document, and this is also true in the three hospital archives in Bergen. In the archive from St. Jørgen’s Hospital, for example, approximately half of the total records consists of various forms of accounting records.

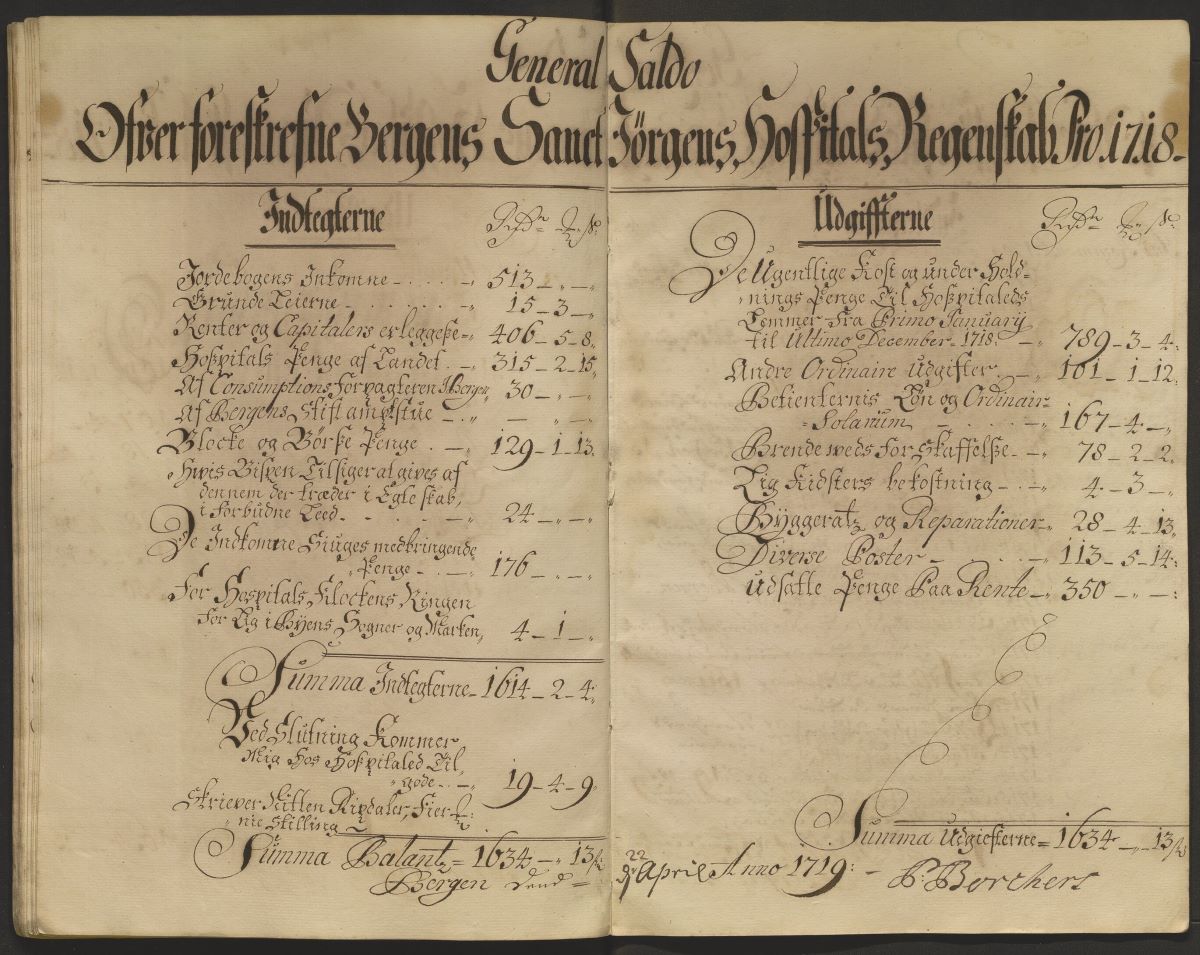

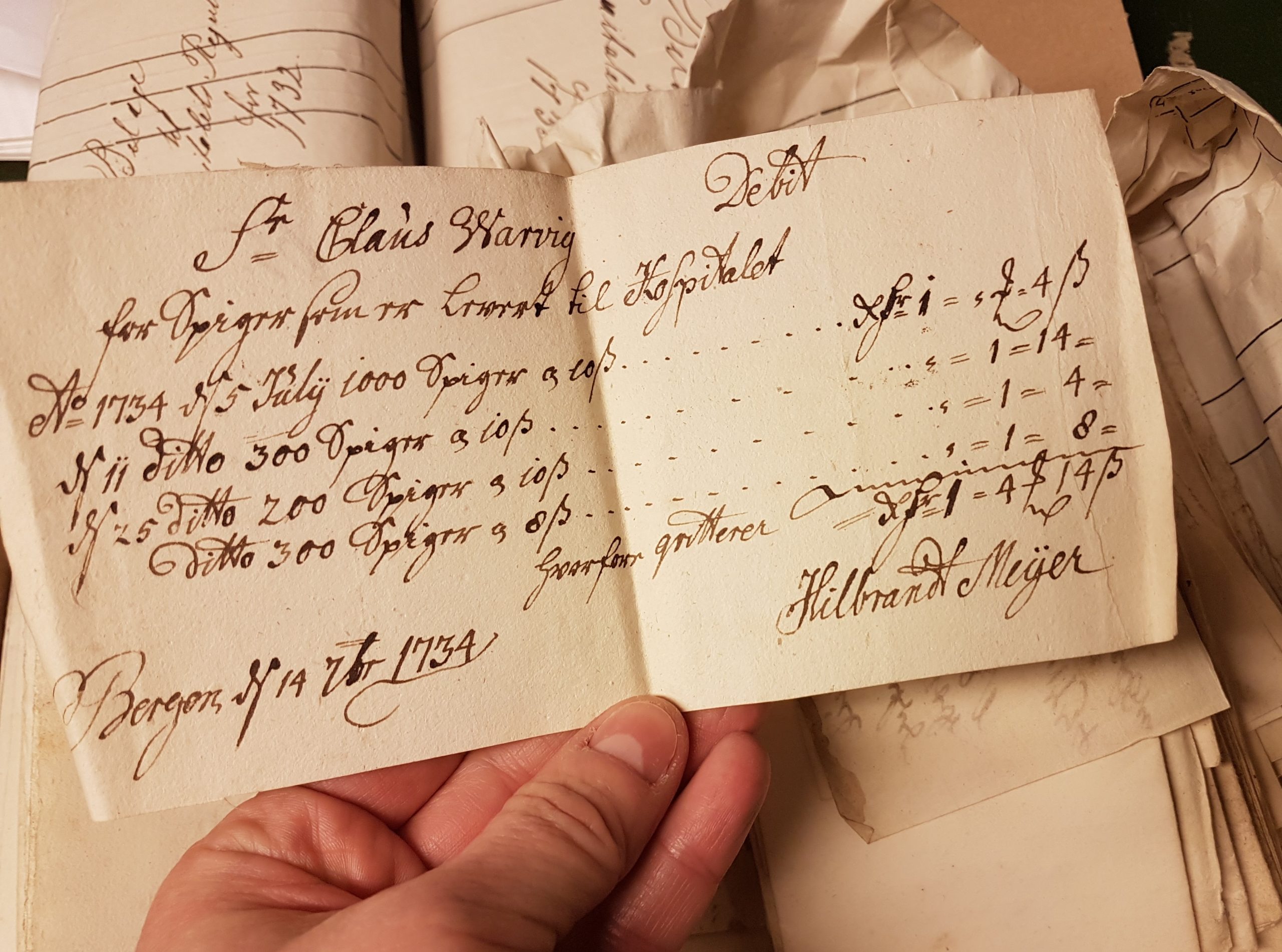

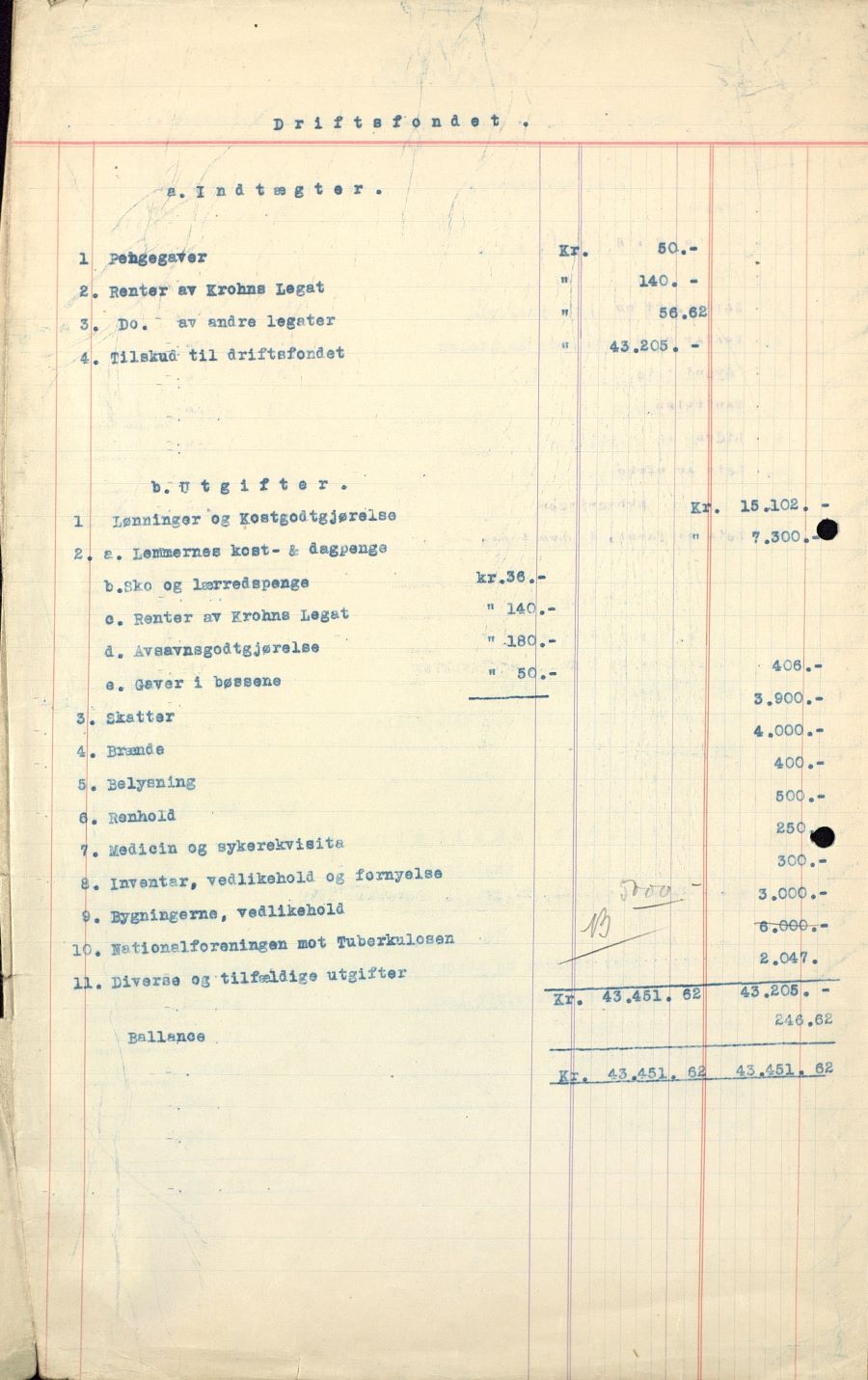

Accounting records often provide important insight about the activities of the hospitals and their associates. They can tell us about the financial conditions at the different hospitals, about income and expenses, and also how they chose to use the funds they had at their disposal.

As a whole, the preserved accounting records are also a rich source of information about life in the hospitals. The preserved 18th-century receipts from St. Jørgen’s Hospital tell us about everything from barn lanterns to communion wine and coffins, while the cash books from the 19th century tell us, among other things, about washing windows and polishing candlesticks. When the accounting ledger from Lungegård Hospital lists the funds used for entertaining patients, it also provides details of how the money was spent, including on a steamship trip, soft drinks and tobacco. Such information about daily life in the hospitals is rarely found in other types of archival material. A number of St. Jørgen’s financial accounts from the 18th century also contain inventory lists, as well as information about the residents. For example, some of the records from this time have copies of letters attached about admission to the hospital.

The oldest accounts from St. Jørgen’s Hospital date from 1687 and can be found in the archive of the county governor in Bergen. A copy of the accounts had to be sent to the county governor, which is why such documentation exists in that archive. It means that if accounts are missing in the hospital’s archive, it may be possible to find them in the county governor’s archive.

The Regional State Archives of Bergen.

Photo: Ingfrid Bækken. Bergen City Archives.

Photo: Ingfrid Bækken. Bergen City Archives.

Bergen City Archives.

The Regional State Archives of Bergen.